Uniswap Foundation × Butter CFM Experiment (July 2025)

This is a qualitative read‑out of the Uniswap Foundation growth CFM #1: what happened in markets, how to interpret it, and what we’ll change next.

Summary

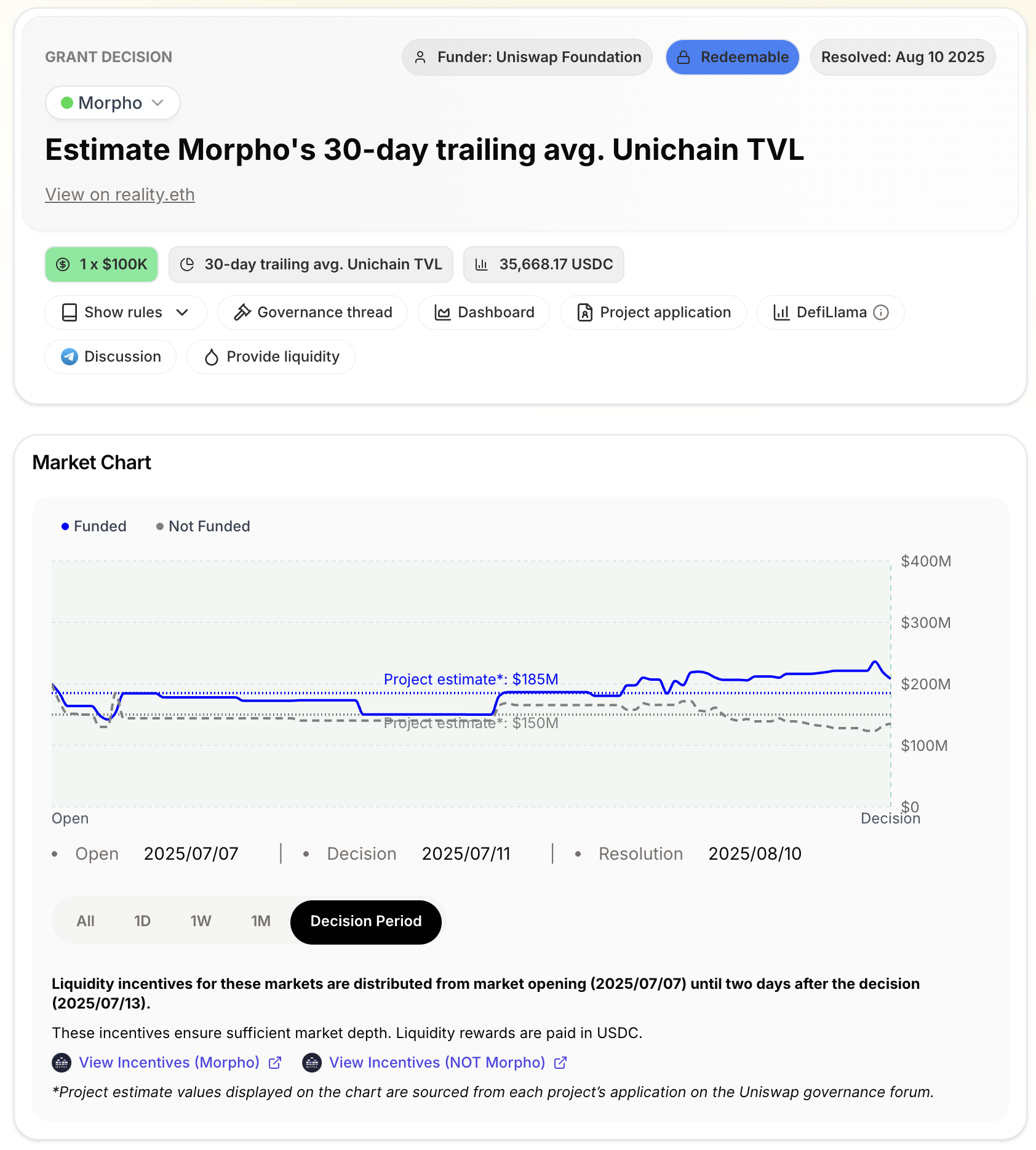

- Winner: Morpho. Grant: $100k USDC.

- Objective (KPI): Grow Unichain TVL. Resolution metric: 30‑day trailing average of Unichain TVL + Borrowed TVL by protocol ending 2025‑08‑10 (UTC) (DeFiLlama).

- Timeline: Markets opened Mon Jul 7 → Decision Fri Jul 11 → KPI resolved Sun Aug 10.

- Decision rule: Capped TWAP around decision (see Butter docs → Process & token flow).

- Liquidity mining (LM): $20k via Merkl on Uniswap v2 (Unichain) from market start → decision + 48h (paid pro‑rata to LP share‑time).

Detailed quantitative report

The companion Hex dashboard holds all statistics relevant for this analysis, including:

- KPI tracking.

- Winner ROI.

- Market evolution, including reversals and decision accuracy.

Refer to the Dune dashboard for on-chain activity.

Key statistics

i. Markets

Relative volumes at decision (Funded branches): Morpho ≈ $19–20k vs Euler ≈ $5.6k, near 4x difference.

Price action on the winner mainly moved one way, while the runner‑up showed more mean‑reversion.

Depth over time: LP depth increased progressively throughout the week until the decision was made.

ii. Decision accuracy

Looking at instant counterfactual spread (Funded − Not Funded) across time, 6 reversals occurred between Morpho and Euler.

Under the capped‑TWAP decision rule, we observe ~1 material reversal event only. Euler’s price remained near its stable value and wasn’t pushed far enough to overturn the TWAP‑based outcome.

Interpretation: price action and volume indicate the presence of significant directional flow on Morpho, together with a certain volume of counter‑manipulative trades.

This report cannot determine whether directional trades were manipulative or whether the market lacked sufficient counter‑manipulative flow.

iii. ROI

Morpho saw a $96.01M increase in the KPI (30-day average Unichain TVL) from start to end of the evaluation period, while the forecasted counterfactual increase was of $67.50M.

This means a raw ROI of 960x: $960 of TVL generated for each $1 invested through the CFM.

This does not account for confounders. Among them, we acknowledge an ETH rally between decision and resolution that lifted USD‑denominated TVL across Unichain.

To account for this, we computed a more modest $7.13 share-ROI based on the increase in Morpho’s relative Unichain TVL share compared to all candidates (refer to the Hex dashboard for details on our methodology). Note that this value still highly depends on other confounders, like ecosystem events.

Determinants of CFM utility

Key insights into the factors that enable or limit CFMs in delivering maximum value to the Funder (in this case, the Uniswap Foundation).

i. KPI alignment (normative lens)

Does the metric reflect the funder’s objective? We optimized for the 30‑day average TVL on Unichain per protocol, which aligns with a growth goal but may over‑weight transient liquidity (see below).

Next step: Introduce an “alignment factor” (meta‑parameter) to evaluate ex‑post to score how well a CFM’s metric captured the funder’s higher‑level goal.

In the rest of this article, we analyze CFMs only in terms of how they directly improve the KPI.

ii. Metric & mechanism issues

There are three main considerations: confounders, time horizon, and manipulation.

Confounders such as macro price moves or ecosystem programs can swamp protocol‑specific effects. Share‑based attribution partly mitigates this but cannot fully isolate causality.

On time horizon, a one-month evaluation period might result in TVL’s lack of stickiness. Running sequential CFMs of 30‑day duration looks like a good answer, but it still optimizes for short‑term growth strategies. It would also be valuable to explore longer‑term horizons.

On manipulation, the decision is made based on the counterfactual delta between Funded and Not Funded branches. This creates two specific risks. First, funded‑branch push, where aligned flow pushes the funded estimate up; counter‑manipulative participation depth is the main defense. Second, not‑funded branch sabotage, in which actions depress the KPI under Not Funded. The most effective version would be a credible commitment to sabotage, enticing traders to price Not‑Funded at zero. We did not observe this here, but it is a design threat. It should ideally be made unprofitable via crypto‑economic/reputational means or by designing a KPI resistant to manipulation (typical solutions: KPI entirely attributable to the Funded case or, on the contrary, ecosystem-level KPI).

As a next step, we intend to model manipulation costs for candidate metrics and estimate projects’ private value of being funded (which drives manipulation propensity). We also aim to design metrics that are inherently costly to game.

iii. Decision accuracy

The goal of a CFM is to allocate funds in the way that best advances the objective, not necessarily to measure a perfect counterfactual ROI. Prediction market inaccuracy is not necessarily a problem when the winner is clear‑cut. However, we need sufficient accuracy and depth (through liquidity deposits or counter‑manipulative flow) to prevent reversals when candidates are close.

Decision selection bias is a secondary concern. Randomized tie‑breaking is a classical mitigation, and in pivotal situations, the uncertainty about final selection already injects implicit randomization. Therefore, we rate selection‑bias risk lower than manipulation risk in this run.

Design levers include experimenting with multi‑winner or split‑allocation rules to reduce “all‑or‑nothing” distortions, and increasing independent trader participation (for example, through adjacent KPI markets that share liquidity and information) to make manipulation costlier and accuracy higher near the margin.

iv. Usefulness of CFMs & next steps

CFMs aim to deliver capture‑resistant funding compared to token voting. Besides parameter‑setting with UF, traders determined the decision in this run, which is a positive operational outcome.

However, decision usefulness should be judged against alternatives. We recommend paired experiments (CFM vs baseline grants/auctions), as done in prior runs, to compare realized ROI across mechanisms. Over time, progressively increasing permissionlessness of the participation/curation layer will also help reduce capture at the proposal stage (see the original design: Conditional Funding Markets).

Recommendations for next CFMs

- Participation & depth. Grow the pool of independent, counter‑manipulative traders; seed adjacent KPI futures to import liquidity and information.

- Metric design. Favor metrics with high manipulation cost and track an alignment factor ex‑post.

- Market rules. Explore multi‑winner or amount‑optimizing rules; explore longer resolution loops where possible.